New FSC analysis demonstrates that the Government’s proposed capital gains tax (CGT) reforms could materially increase taxes on Australians investing outside superannuation, including younger Australians, families, part-time workers and Australians approaching retirement.

Under the announced changes, the existing 50 per cent CGT discount for individuals, trusts and partnerships would be replaced with a system of cost-base indexation and a new 30 per cent minimum tax applying to capital gains accruing after 1 July 2027.

FSC modelling indicates the changes will increase the effective tax rate on long-term investments in shares, ETFs and managed funds, where long-run investment returns materially exceed inflation.

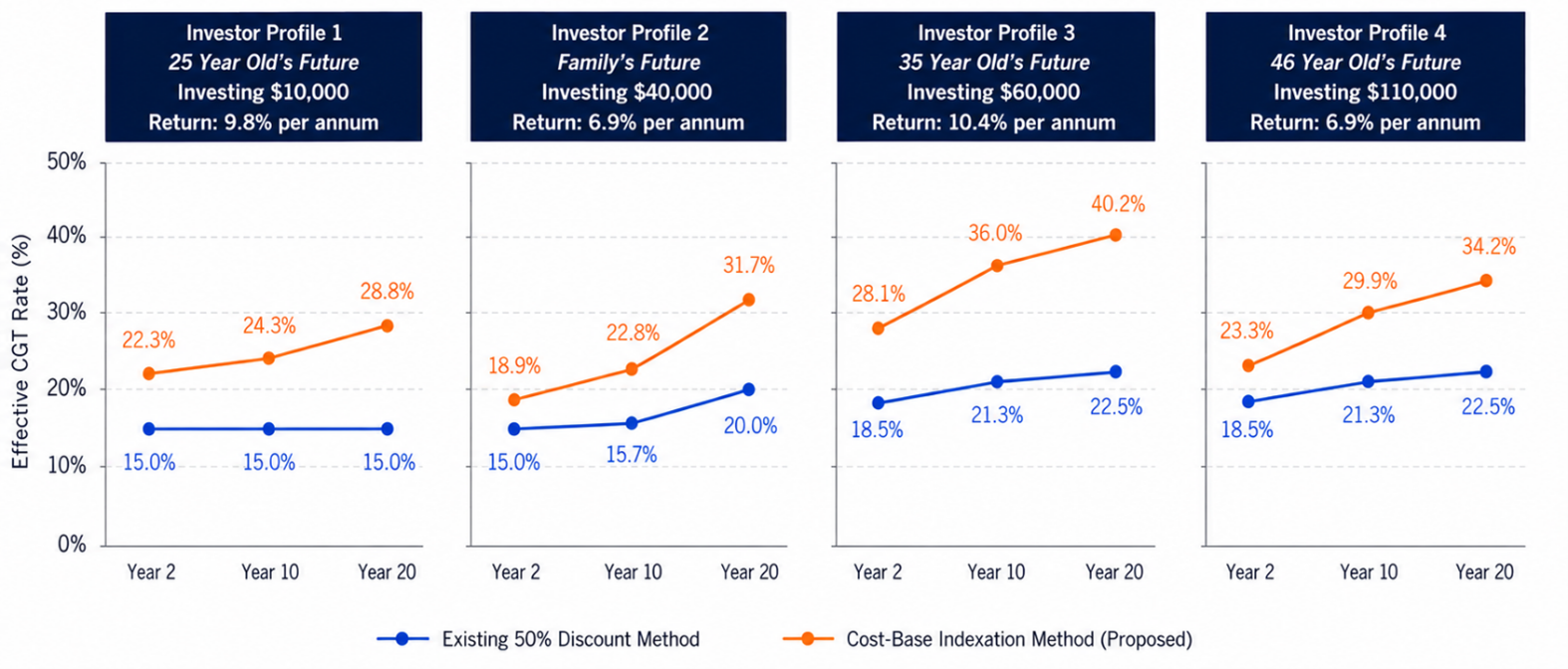

Investor Profile Analysis

Under the FSC’s modelling:

- A 25-year-old Australian on the median income investing $10,000 in Australian shares would pay an additional $151 in tax after 2 years, $1,443 after 10 years and $7,552 after 20 years under the proposed framework. Over that period, the effective CGT rate would rise from 15 per cent under the current 50 per cent discount to 28.8 per cent under the proposed cost-base indexation model.

- A median-income young family investing $40,000 in a balanced managed fund would pay an additional $13,106 in tax after 20 years, with the effective CGT rate increasing from 22.5 per cent to 31.7 per cent.

- A 35-year-old professional on an above-median income investing $60,000 in a high-growth managed fund would pay an additional $66,045 in tax after 20 years, with the effective CGT rate rising from 22.5 per cent to 40.2 per cent.

- A 46-year-old operations manager on an above-median income investing $110,000 to build financial security would pay an additional $36,042 in tax after 20 years under the proposed framework, with the effective CGT rate increasing from 22.5 per cent to 34.2 per cent.

Effective CGT Rates Over Time Under Proposed CGT Regime*

*Effective CGT Rate is the total CGT paid as a percentage of the gross capital gain. Outcomes based in assumptions as outlined above and under each profile in the Fact Sheet.

Two ‘Investor Profiles’ also demonstrate the impact of the proposed 30 per cent minimum tax on capital gains on Australians who are in lower income brackets, including students, part-time workers, carers and Australians easing into retirement. The new minimum tax will override the normal operation of lower marginal tax brackets by imposing a 30 per cent floor on investment gains.

For people on low incomes, FSC’s modelling shows:

- After just two years, a 19-year-old student working part-time and investing $15,000 in a diversified ETF portfolio, would see their effective CGT rate almost triple – rising from 7 per cent under the current 50 per cent discount to 19.1 per cent under the proposed cost-base indexation method.

- A 53-year-old who has involuntarily reduced their hours to part-time work, due to a redundancy ahead of retirement, would see the tax payable on a $15,000 real capital gain increase from $1,050 to $4,500 solely because of the proposed minimum tax floor.

The ‘Investor Profiles’ modelled in this analysis assume investments generate meaningful real capital growth over time, consistent with long-term historical returns for the asset classes examined.

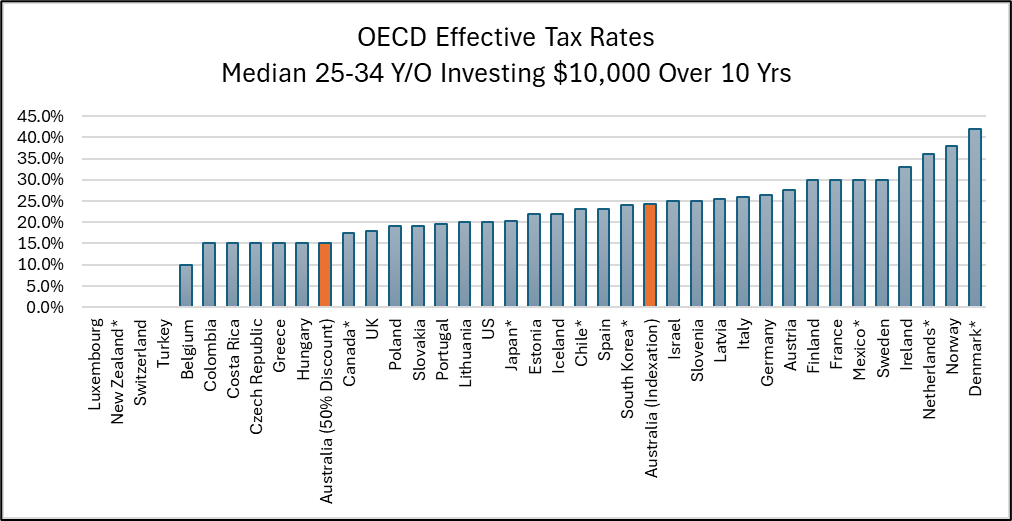

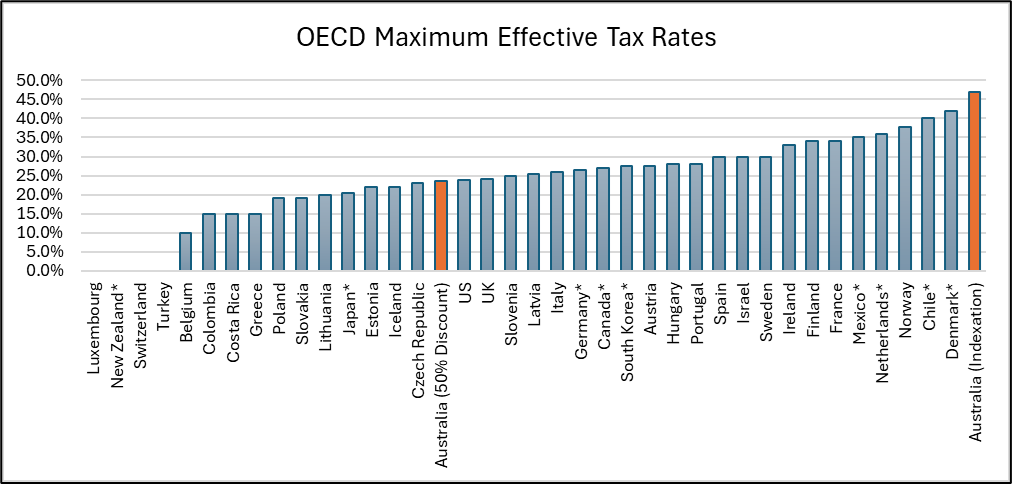

International Benchmarking

The FSC’s modelling indicates the reforms risk undermining Australia’s international competitiveness by materially increasing effective CGT rates relative to other OECD economies.

Under the current system, Australia has the sixth lowest effective CGT rate in the OECD for a median 25-34 year-old investing $10,000 in shares over 10 years. Under the proposed framework, Australia would fall to 24th lowest.

The changes shift Australia from having one of the more internationally competitive CGT regimes, to the lower half of the OECD rankings.

At the upper end, Australia could potentially face the highest effective CGT regime in the OECD, with effective rates rising toward 47 per cent depending on investment performance and inflation outcomes.

Data Source

The FSC’s analysis is based on the Government’s announced Budget 2026-27 CGT reforms, Treasury fact sheet examples, Australian Bureau of Statistics median earnings data, public managed fund and share market historical return data, OECD capital gains tax settings, and publicly available international tax information.

Assumptions

- Assets are purchased from 1 July 2027 and held continuously for the periods identified, to isolate the tax implications of the new cost-base indexation model.

- Inflation – 2.6% per annum, based on the ATO’s reference CPI Index between 30 June 1995 and 30 June 2025. Treasury also forecasts CPI to average 2.5 per cent per annum from 1 July 2027.

- Investment return assumptions are specified for each investor profile and based on publicly available historical return data.

- Incomes based on existing ABS median earnings would likely be higher by 1 July 2027.

- Income estimates also incorporate the effects of bracket creep by applying inflation-indexed estimates of future income levels.

- The income estimates are therefore likely to understate the actual tax liabilities, particularly as earnings typically increase over an individual’s working life to 55 years old.

- Medicare levy impacts and tax offsets are excluded for simplicity.

- International comparisons assume the investor is a resident taxpayer investing from their domestic jurisdiction. Assets sold are shares. Effective tax rates reflect the country’s current domestic tax settings and do not project future legislative changes, indexation, deductions, exemptions or carried-forward losses.

- ENDS –

Media Contact: Bronwyn Allan – 0421 506 231 – This email address is being protected from spambots. You need JavaScript enabled to view it.

About the Financial Services Council

The FSC is a peak body which sets mandatory Standards and develops policy for more than 130 member companies in one of Australia’s largest industry sectors, financial services. Our Full Members represent Australia’s retail and wholesale funds management businesses, superannuation funds, and financial advice licensees. Our Supporting Members represent the professional services firms such as ICT, consulting, accounting, legal, recruitment, actuarial and research houses. The financial services industry is responsible for investing more than $4 trillion on behalf of over 16.9 million Australians. The pool of funds under management is larger than Australia’s GDP and the capitalisation of the Australian Securities Exchange and is one of the largest pools of managed funds in the world.